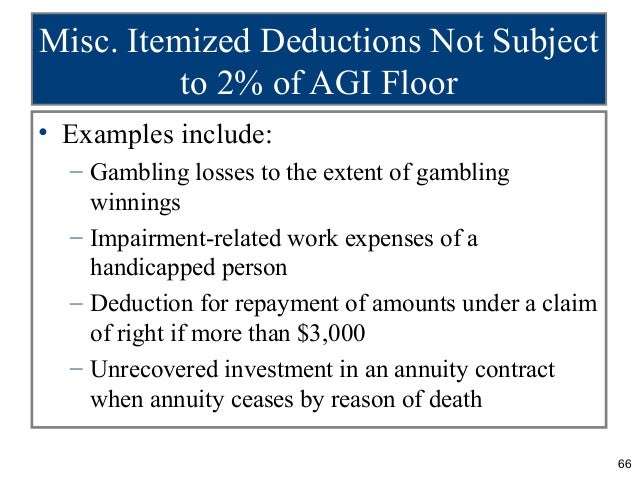

Deductions Not Subject To The 2 Floor

Form W 11 Number 11 11 Common Mistakes Everyone Makes In Form W 11 Number 11 Form W 11 Number 11 11 Common Mistakes Everyone Makes In For How To Get Money Irs

Vol 01 Chapter 10 2015

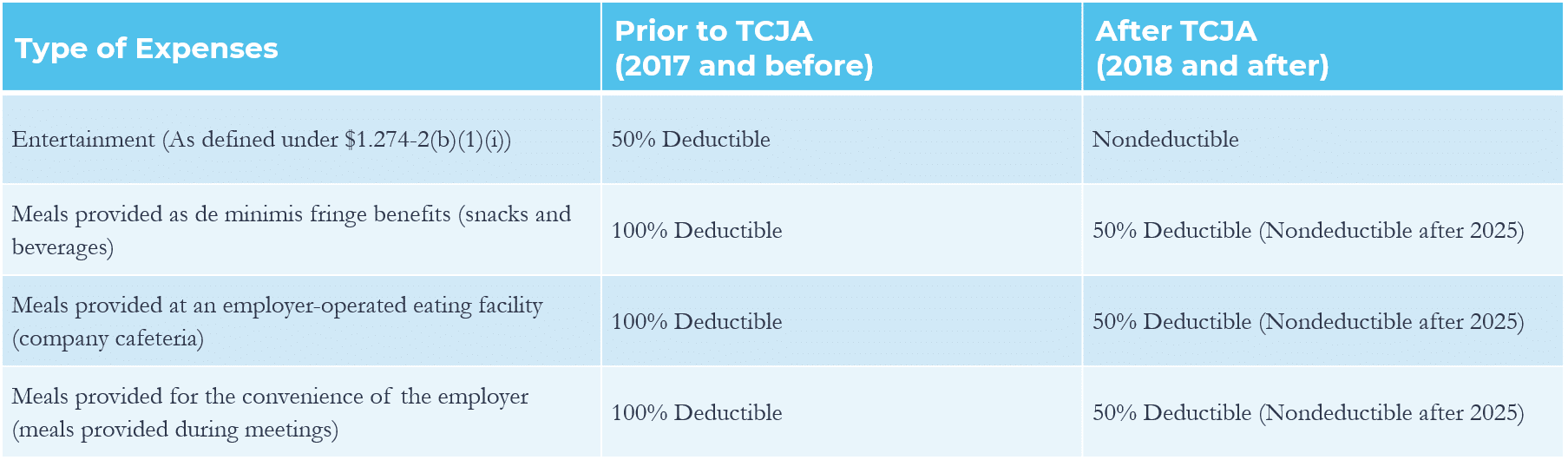

Navigating The New Meals And Entertainment Deductions Under Tcja Grf Cpas Advisors

To Know The Tax Benefits Provided To First Time Home Buyers Watch Out Image Below To Grab These Benefits Just Call Out 8852 Finance Loans Loan Investing

Tax Benefits Are Just One Of The Awesome Advantages Of Having Your Own Home Based Business The Home Based Business Successful Home Business Internet Business

Acct 426 Tax I Chapter 10 Flashcards Quizlet

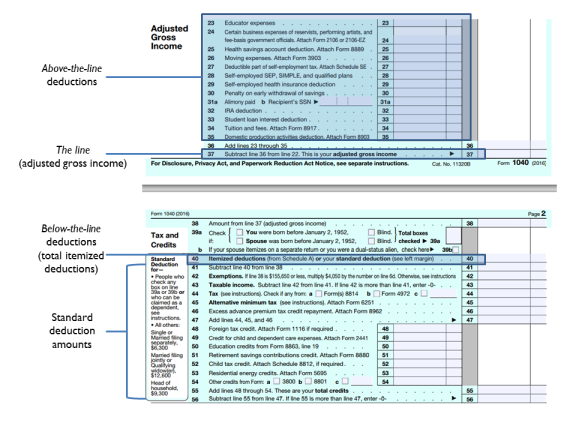

1000 100 50 1150 line 23 of schedule a figure 2 of his agi.

Deductions not subject to the 2 floor.

Tax Deductions For Individuals A Summary Everycrsreport Com

Potential Tax Benefits With Images Disabled Children Williams Syndrome Parenting

Check Out All The Things Educators Can Deduct From Their Taxes Save Those Hard Earned Dollars Teache Teacher Tax Deductions First Year Teaching Teacher Info

Acct 421 Chapter 9 Flashcards Quizlet

Source : pinterest.com